|

Frequently Asked Questions:

First Time Home Buyer Tax Credit of $8,000

1. Who is eligible to claim the tax credit?

First-time home buyers purchasing any kind of home—new or resale—are eligible for the tax credit. To qualify for the tax credit, a home purchase must occur on or after January 1, 2009 and before December 1, 2009. For the purposes of the tax credit, the purchase date is the date when closing occurs and the title to the property transfers to the home owner.

2. What is the definition of a first-time home buyer?

The law defines "first-time home buyer" as a buyer who has not owned a principal residence during the three-year period prior to the purchase. For married taxpayers, the law tests the homeownership history of both the home buyer and his/her spouse.

For example, if you have not owned a home in the past three years but your spouse has owned a principal residence, neither you nor your spouse qualifies for the first-time home buyer tax credit. However, unmarried joint purchasers may allocate the credit amount to any buyer who qualifies as a first-time buyer, such as may occur if a parent jointly purchases a home with a son or daughter. Ownership of a vacation home or rental property not used as a principal residence does not disqualify a buyer as a first-time home buyer.

3. How is the amount of the tax credit determined?

The tax credit is equal to 10 percent of the home’s purchase price up to a maximum of $8,000.

4. Are there any income limits for claiming the tax credit?

The tax credit amount is reduced for buyers with a modified adjusted gross income (MAGI) of more than $75,000 for single taxpayers and $150,000 for married taxpayers filing a joint return. The tax credit amount is reduced to zero for taxpayers with MAGI of more than $95,000 (single) or $170,000 (married) and is reduced proportionally for taxpayers with MAGIs between these amounts.

5. What is "modified adjusted gross income"?

Modified adjusted gross income or MAGI is defined by the IRS. To find it, a taxpayer must first determine "adjusted gross income" or AGI. AGI is total income for a year minus certain deductions (known as "adjustments" or "above-the-line deductions"), but before itemized deductions from Schedule A or personal exemptions are subtracted. On Forms 1040 and 1040A, AGI is the last number on page 1 and first number on page 2 of the form. For Form 1040-EZ, AGI appears on line 4 (as of 2007). Note that AGI includes all forms of income including wages, salaries, interest income, dividends and capital gains.

To determine modified adjusted gross income (MAGI), add to AGI certain amounts such as foreign income, foreign-housing deductions, student-loan deductions, IRA-contribution deductions and deductions for higher-education costs.

6. If my modified adjusted gross income (MAGI) is above the limit, do I qualify for any tax credit?

Possibly. It depends on your income. Partial credits of less than $8,000 are available for some taxpayers whose MAGI exceeds the phase-out limits.

7. Can you give me an example of how the partial tax credit is determined?

Just as an example, assume that a married couple has a modified adjusted gross income of $160,000. The applicable phase out to qualify for the tax credit is $150,000, and the couple is $10,000 over this amount. Dividing $10,000 by $20,000 yields 0.5. When you subtract 0.5 from 1.0, the result is 0.5. To determine the amount of the partial first-time home buyer tax credit that is available to this couple, multiply $8,000 by 0.5. The result is $4,000.

Here’s another example: assume that an individual home buyer has a modified adjusted gross income of $88,000. The buyer’s income exceeds $75,000 by $13,000. Dividing $13,000 by $20,000 yields 0.65. When you subtract 0.65 from 1.0, the result is 0.35. Multiplying $8,000 by 0.35 shows that the buyer is eligible for a partial tax credit of $2,800.

Please remember that these examples are intended to provide a general idea of how the tax credit might be applied in different circumstances. You should always consult your tax advisor for information relating to your specific circumstances.

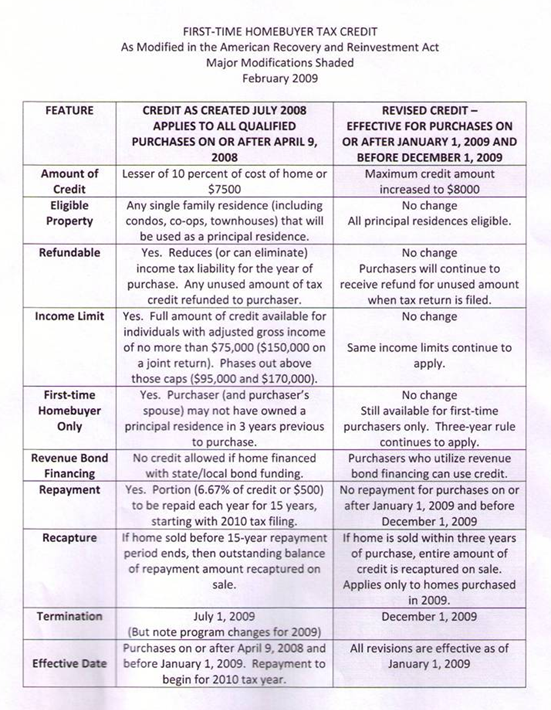

8. How is this home buyer tax credit different from the tax credit that Congress enacted in July of 2008?

The most significant difference is that this tax credit does not have to be repaid. Because it had to be repaid, the previous "credit" was essentially an interest-free loan. This tax incentive is a true tax credit. However, home buyers must use the residence as a principal residence for at least three years or face recapture of the tax credit amount. Certain exceptions apply.

9. How do I claim the tax credit? Do I need to complete a form or application?

Participating in the tax credit program is easy. You claim the tax credit on your federal income tax return. Specifically, home buyers should complete IRS Form 5405 to determine their tax credit amount, and then claim this amount on Line 69 of their 1040 income tax return. No other applications or forms are required, and no pre-approval is necessary. However, you will want to be sure that you qualify for the credit under the income limits and first-time home buyer tests.

10. What types of homes will qualify for the tax credit?

Any home that will be used as a principal residence will qualify for the credit. This includes single-family detached homes, attached homes like townhouses and condominiums, manufactured homes (also known as mobile homes) and houseboats. The definition of principal residence is identical to the one used to determine whether you may qualify for the $250,000 / $500,000 capital gain tax exclusion for principal residences.

11. I read that the tax credit is "refundable." What does that mean?

The fact that the credit is refundable means that the home buyer credit can be claimed even if the taxpayer has little or no federal income tax liability to offset. Typically this involves the government sending the taxpayer a check for a portion or even all of the amount of the refundable tax credit.

For example, if a qualified home buyer expected, notwithstanding the tax credit, federal income tax liability of $5,000 and had tax withholding of $4,000 for the year, then without the tax credit the taxpayer would owe the IRS $1,000 on April 15th. Suppose now that the taxpayer qualified for the $8,000 home buyer tax credit. As a result, the taxpayer would receive a check for $7,000 ($8,000 minus the $1,000 owed).

12. I purchased a home in early 2009 and have already filed to receive the $7,500 tax credit on my 2008 tax returns. How can I claim the new $8,000 tax credit instead?

Home buyers in this situation may file an amended 2008 tax return with a 1040X form. You should consult with a tax advisor to ensure you file this return properly.

13. Instead of buying a new home from a home builder, I hired a contractor to construct a home on a lot that I already own. Do I still qualify for the tax credit?

Yes. For the purposes of the home buyer tax credit, a principal residence that is constructed by the home owner is treated by the tax code as having been "purchased" on the date the owner first occupies the house. In this situation, the date of first occupancy must be on or after January 1, 2009 and before December 1, 2009.

In contrast, for newly-constructed homes bought from a home builder, eligibility for the tax credit is determined by the settlement date.

14. Can I claim the tax credit if I finance the purchase of my home under a mortgage revenue bond (MRB) program?

Yes. The tax credit can be combined with the MRB home buyer program. Note that first-time home buyers who purchased a home in 2008 may not claim the tax credit if they are participating in an MRB program.

15. I live in the District of Columbia. Can I claim both the Washington, D.C. first-time home buyer credit and this new credit?

No. You can claim only one.

16. I am not a U.S. citizen. Can I claim the tax credit?

Maybe. Anyone who is not a nonresident alien (as defined by the IRS), who has not owned a principal residence in the previous three years and who meets the income limits test may claim the tax credit for a qualified home purchase. The IRS provides a definition of "nonresident alien" in IRS Publication 519.

17. Is a tax credit the same as a tax deduction?

No. A tax credit is a dollar-for-dollar reduction in what the taxpayer owes. That means that a taxpayer who owes $8,000 in income taxes and who receives an $8,000 tax credit would owe nothing to the IRS.

A tax deduction is subtracted from the amount of income that is taxed. Using the same example, assume the taxpayer is in the 15 percent tax bracket and owes $8,000 in income taxes. If the taxpayer receives an $8,000 deduction, the taxpayer’s tax liability would be reduced by $1,200 (15 percent of $8,000), or lowered from $8,000 to $6,800.

18. I bought a home in 2008. Do I qualify for this credit?

No, but if you purchased your first home between April 9, 2008 and January 1, 2009, you may qualify for a different tax credit.

19. Is there any way for a home buyer to access the money allocable to the credit sooner than waiting to file their 2009 tax return?

Yes. Prospective home buyers who believe they qualify for the tax credit are permitted to reduce their income tax withholding. Reducing tax withholding (up to the amount of the credit) will enable the buyer to accumulate cash by raising his/her take home pay. This money can then be applied to the down payment.

Buyers should adjust their withholding amount on their W-4 via their employer or through their quarterly estimated tax payment. IRS Publication 919 contains rules and guidelines for income tax withholding. Prospective home buyers should note that if income tax withholding is reduced and the tax credit qualified purchase does not occur, then the individual would be liable for repayment to the IRS of income tax and possible interest charges and penalties.

Further, rule changes made as part of the economic stimulus legislation allow home buyers to claim the tax credit and participate in a program financed by tax-exempt bonds. Some state housing finance agencies, such as the Missouri Housing Development Commission, have introduced programs that provide short-term credit acceleration loans that may be used to fund a down payment. Prospective home buyers should inquire with their state housing finance agency to determine the availability of such a program in their community.

20. If I’m qualified for the tax credit and buy a home in 2009, can I apply the tax credit against my 2008 tax return?

Yes. The law allows taxpayers to choose ("elect") to treat qualified home purchases in 2009 as if the purchase occurred on December 31, 2008. This means that the 2008 income limit (MAGI) applies and the election accelerates when the credit can be claimed (tax filing for 2008 returns instead of for 2009 returns). A benefit of this election is that a home buyer in 2009 will know their 2008 MAGI with certainty, thereby helping the buyer know whether the income limit will reduce their credit amount.

Taxpayers buying a home who wish to claim it on their 2008 tax return, but who have already submitted their 2008 return to the IRS, may file an amended 2008 return claiming the tax credit. You should consult with a tax professional to determine how to arrange this.

21. For a home purchase in 2009, can I choose whether to treat the purchase as occurring in 2008 or 2009, depending on in which year my credit amount is the largest?

Yes. If the applicable income phase-out would reduce your home buyer tax credit amount in 2009 and a larger credit would be available using the 2008 MAGI amounts, then you can choose the year that yields the largest credit amount.

|