Home Updates that Pay When You Sell

Thursday, February 27, 2025

Add Comment

Displaying blog entries 1-8 of 8

Are you having a hard time finding the right home in your budget? Or maybe you already own a home but could use some extra income or a designated space for aging loved ones. Either way, accessory dwelling units (ADUs) could be the smart solution you’ve been looking for in today’s market.

According to Fannie Mae, an ADU is a small, separate living space that’s on the same lot as a single-family home. It must include its own areas for living, sleeping, cooking, and bathrooms independent of the main house. And they can take shape in a few different ways. Fannie Mae adds, an ADU can be:

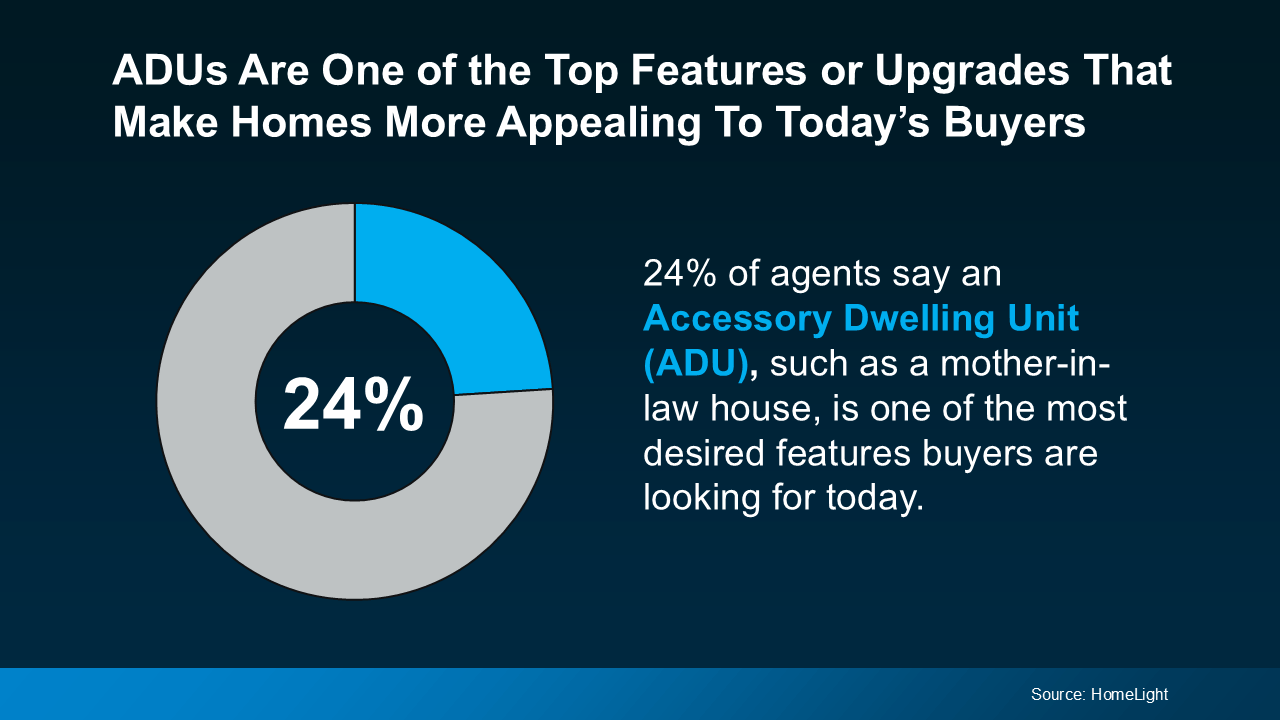

ADUs are growing in popularity as more people discover why they’re so practical. In fact, a recent survey shows that 24% of agents say an ADU, such as a mother-in-law house, is one of the most desired features buyers are looking for right now.

The growing appeal makes sense. With rising costs all around you, an ADU can help supplement your income and ease some of the strain on your wallet. Whether you buy a home that has one already or you add one on, it gives you the option to rent out that portion of your home to help pay your mortgage.

The growing appeal makes sense. With rising costs all around you, an ADU can help supplement your income and ease some of the strain on your wallet. Whether you buy a home that has one already or you add one on, it gives you the option to rent out that portion of your home to help pay your mortgage.

Here are some of the other top benefits of ADUs, according to Freddie Mac and the AARP:

It’s worth noting that since an ADU exists on a single-family lot as a secondary dwelling, it typically can’t be sold separately from the primary residence. And while that’s changing in some states, regulations vary by location. So, connect with a local real estate expert for the most up-to-date guidance.

In today’s market, buying a home with an ADU or adding one to your current house could be worth considering. Just be sure to talk with a real estate agent who can explain local codes and regulations for this type of housing and what’s available in your area.

What’s your motivation for exploring ADUs?

It feels like everything is getting more expensive these days. That’s because inflation has remained higher than normal for longer than expected – and that’s impacting the costs of goods, services, and more. And with rising costs all around you, you’re probably questioning: is now really the right time to buy a home?

Here’s the good news. Owning a home is actually one of the best ways to protect yourself from the rising costs that come with inflation.

One of the key benefits of homeownership is that when you buy a home with a fixed-rate mortgage, your biggest monthly expense — your mortgage payment — stabilizes. Sure, your payment could rise slightly as your homeowner’s insurance and property taxes shift. But no matter what happens with inflation, your principal and interest payments won’t change.

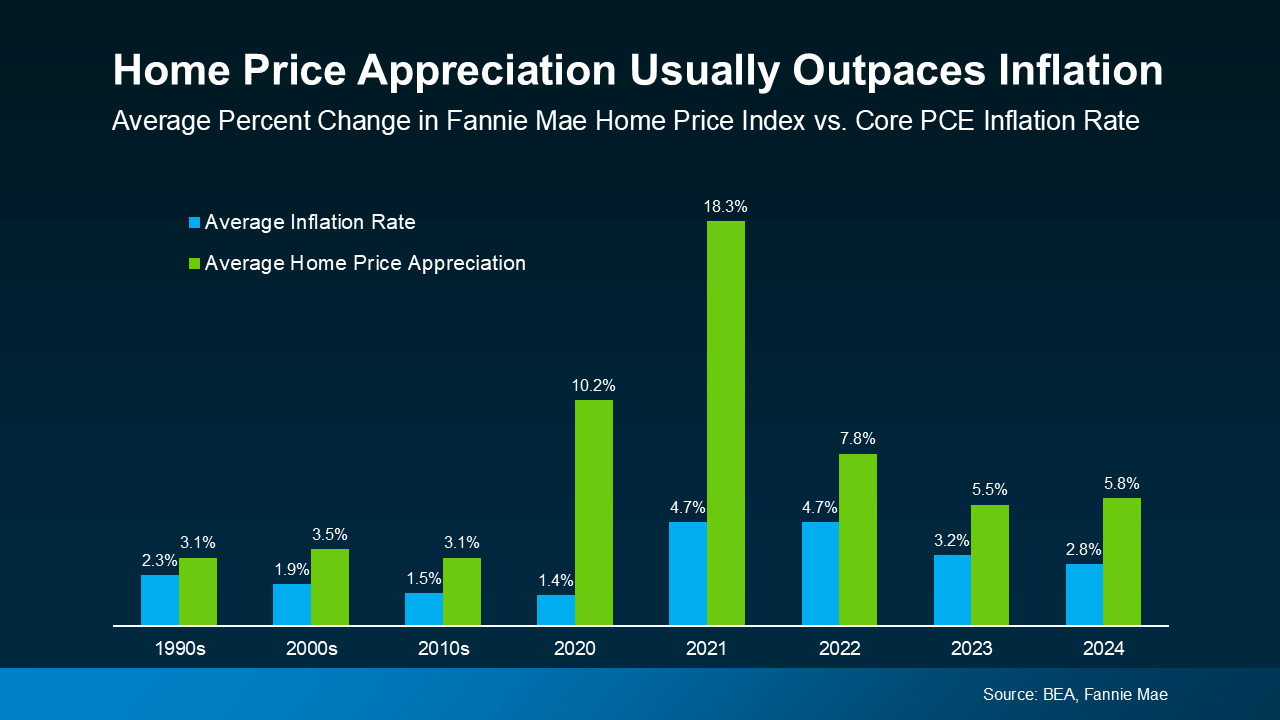

That’s not the case if you rent. Rent tends to rise over time, and it usually goes up even faster than the rate of inflation. Just look at the data from the Bureau of Economic Analysis (BEA) and the Census Bureau (see graph below):

So, while renters face higher costs year after year, homeowners with a fixed mortgage rate lock in their monthly payments, making it easier to budget no matter what happens with inflation.

So, while renters face higher costs year after year, homeowners with a fixed mortgage rate lock in their monthly payments, making it easier to budget no matter what happens with inflation.

Another big reason homeownership is a great hedge against inflation is that home values tend to appreciate over time — often at a higher rate than inflation, according to data from the BEA and Fannie Mae (see graph below):

That makes real estate one of the strongest long-term investments during times of rising prices. While inflation can chip away at the value of cash savings, real estate typically holds or grows in value, allowing you to build wealth.

That makes real estate one of the strongest long-term investments during times of rising prices. While inflation can chip away at the value of cash savings, real estate typically holds or grows in value, allowing you to build wealth.

On the other hand, renting offers no protection against inflation. In fact, it does the opposite — when inflation drives up costs, landlords often pass those increases onto tenants through higher rents.

That means as a renter, you’re continually paying more without gaining any financial benefit. But as a homeowner, rising prices work in your favor by increasing the value of your home and growing your equity over time.

And with experts forecasting continued home price growth, that means you’re making an investment that usually grows in value and should outperform inflation in the years ahead.

In short, a fixed-rate mortgage protects your budget, and home price appreciation grows your net worth. That’s why homeownership is a strong hedge against inflation.

Inflation can make everyday expenses unpredictable, but owning a home gives you stability. Unlike rent, your monthly mortgage payment stays pretty much the same over time. Plus, the value of your home is likely to increase after you buy.

How would having a fixed housing payment change the way you budget for the future?

Some homeowners hesitate to sell because they’ve got unanswered questions that hold them back. But a lot of times their concerns are based on misconceptions, not facts. And if they’d just talk to an agent about it, they’d see these doubts aren’t necessarily a hurdle at all.

If uncertainty is keeping you from making a move, it’s time to get the real answers. The ones you deserve. And to take the pressure off, you don’t have to ask the questions, because here’s the data that answers them.

If you own a home already, you may be tempted to wait because you don’t want to sell and take on a higher mortgage rate on your next house. But your move may be a lot more feasible than you think, and that’s because of how much your house has likely grown in value.

Think about it. Do you know anyone in your neighborhood who’s sold their house recently? If so, did you hear what it sold for? With how much home values have gone up in recent years, the number may surprise you. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), the typical homeowner has gained $147,000 in housing wealth in the last five years alone.

That’s significant – and when you sell, that can give you what you need to fund your next move.

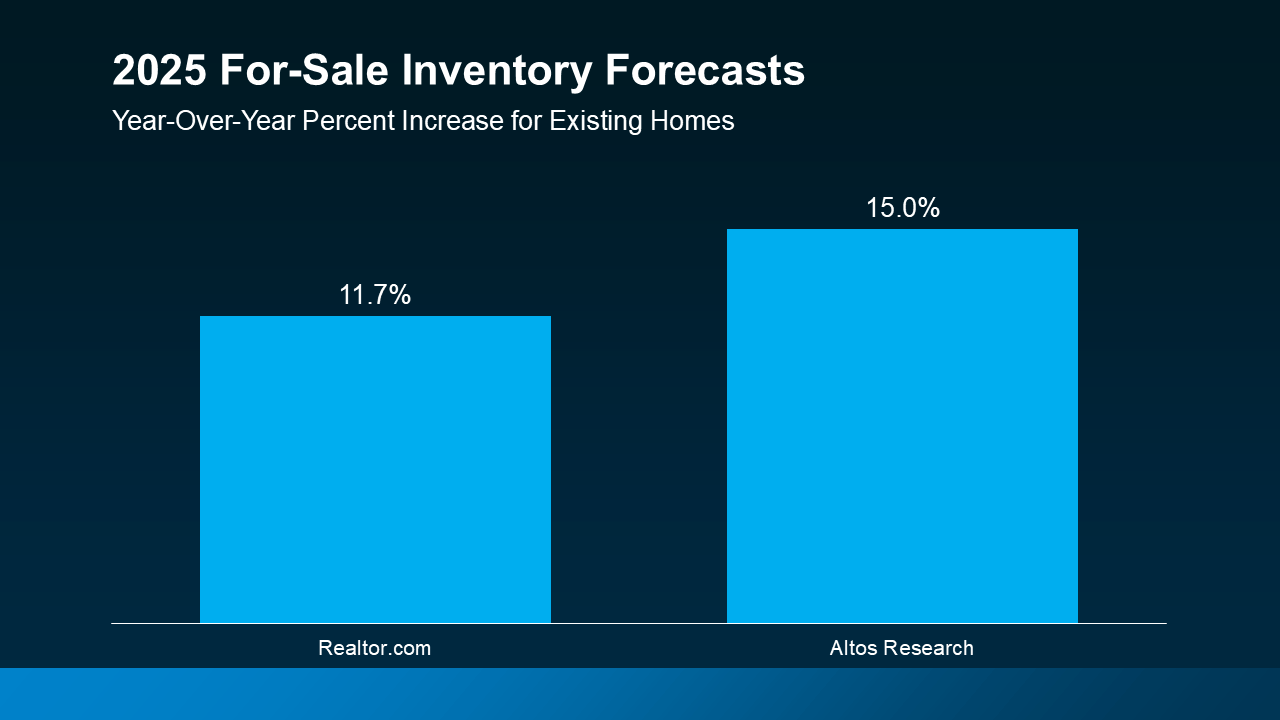

If this is on your mind, it’s probably because you remember just how hard it was to find a home over the past few years. But in today’s market, it isn’t as challenging.

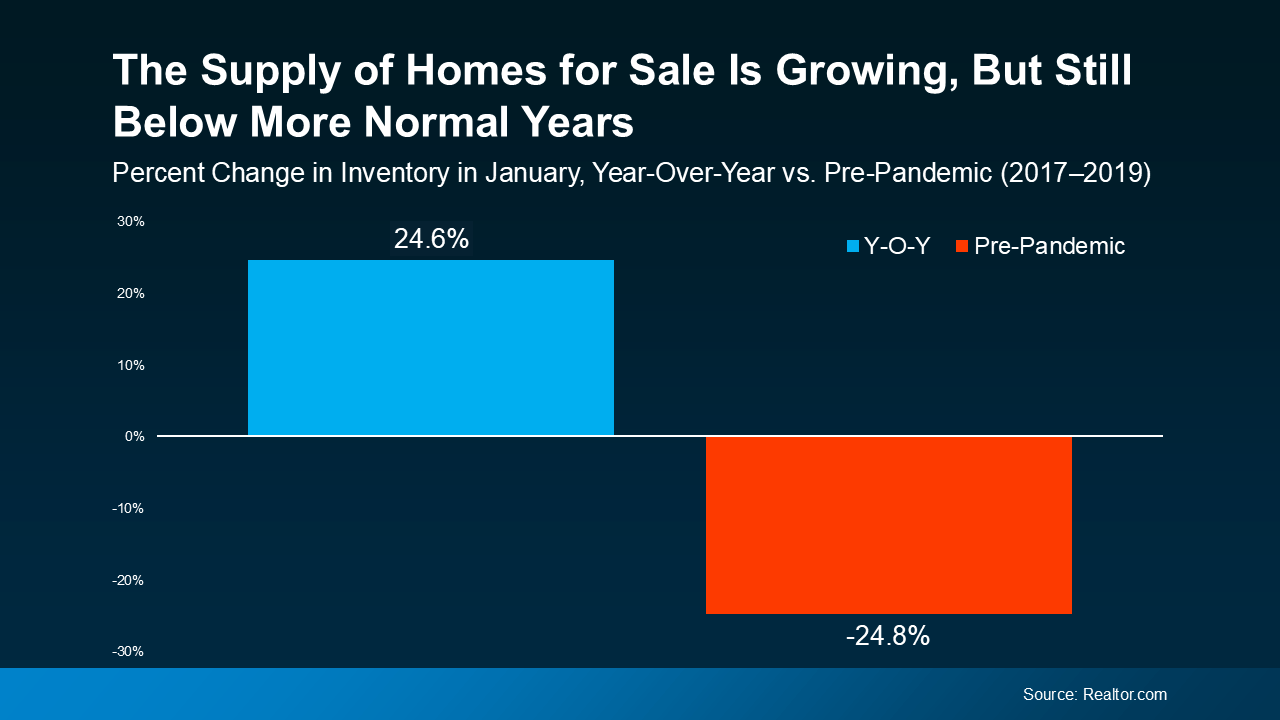

Data from Realtor.com shows how much inventory has increased – it's up nearly 25% compared to this time last year (see graph below):

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

And last, if you’re worried no one’s buying with rates and prices where they are right now, here’s some perspective that can help. While there weren’t as many home sales last year as there’d be in a normal market, roughly 4.24 million homes still sold (not including new construction), according to the National Association of Realtors (NAR). And the expectation is that number will rise in 2025. But even if we only match how many homes sold last year, here’s what that looks like.

Think about that. Just in the time it took you to read this, 8 homes sold. Let this reassure you – the market isn’t at a standstill. Every day, thousands of people buy, and they're looking for homes like yours.

When you’re ready to walk through what’s on your mind, I have the answers you need. And in the meantime, tell me: what’s holding you back from making your move?

Spring is the busiest season in the housing market. It’s the time of year when buyers are most active – that means it’s when homes sell faster and for top dollar. If you’ve already got a move on your mind, why not list this spring and take advantage of the added buyer demand?

Since spring is just around the corner, now’s the time to start getting your house market-ready. You’ve got just over a month to do the prep work. And while that may sound like a decent amount of time, it’s going to go by quickly. And you won’t want to rush through this important task – especially this year.

Right now, two things are true. There are more homes on the market than there have been in years. And buyers are being extra selective. That combination means you need to invest some time and effort in making strategic repairs. And many homeowners already have a jump on this work.

In the 2025 Outlook for Home Remodeling, Carlos Martin, Director of the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, explains:

“. . . homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.”

And the most common projects they’re tackling are replacing water heaters, HVAC units, and flooring. Energy efficiency is a key consideration too, based on home improvement data from the Census.

But just because that’s what other homeowners are doing, it doesn’t mean that’s what you have to tackle. Think about what you’d want to see if you were a buyer. Focus on quick wins that are easy to knock out with the time you have – but, don’t ignore key repairs, especially ones you think could turn off buyers.

While big-ticket items like replacing an old roof or outdated flooring may seem daunting, they can pay off – especially if you focus on projects with the best return on investment (ROI).

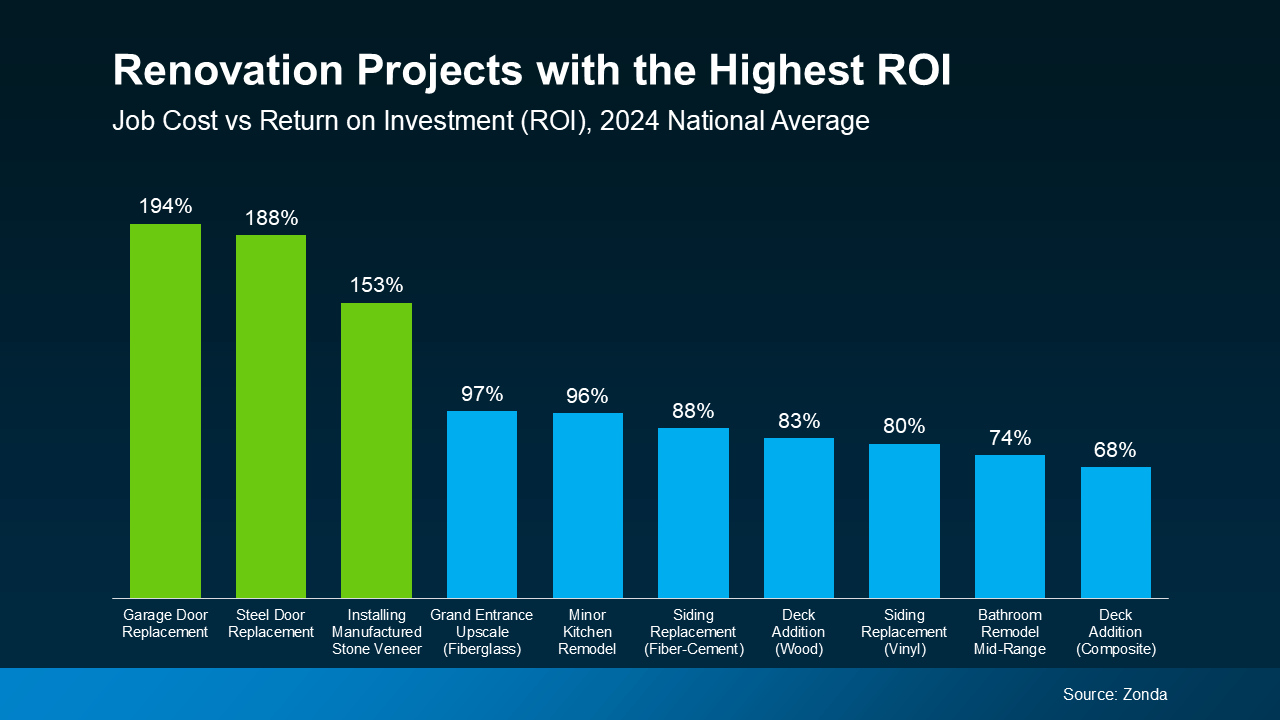

An agent’s expertise is key in narrowing down your list to what’s actually worth it. They know what buyers in your area want and they also have data like this report from Zonda to guide you on which updates have the best ROI (see green in the graph below):

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

“As a seller, it’s smart to be prepared and control whatever factors you’re able to. Things like hiring a great real estate agent and maximizing your home’s online appeal can translate into a smoother sale — and more money in the bank.”

It’s not too early to partner with an agent. By starting now, you’ve still got time to space out the work and find any contractors you need to get the job done. If you wait until spring to roll up your sleeves, you risk running out of time – and that means your house may be overshadowed by others who are more buyer-ready.

If you’re planning to sell this spring, it’s time to start tackling your to-do list. But, before you get started, let’s connect. That way you can make sure you’re spending your time and budget on projects that’ll pay off in the long run.

Send me a list of what’s on your to-do list, and we can prioritize them together.

If you want to sell your house, having the right strategies and expectations is key. But some sellers haven’t adjusted to where the market is today. They’re not factoring in that there are more homes for sale or that buyers are being more selective with their budgets. And those sellers are making some costly mistakes.

Here’s a quick rundown of the 3 most common missteps sellers are making, and how partnering with an expert agent can help you avoid every single one of them.

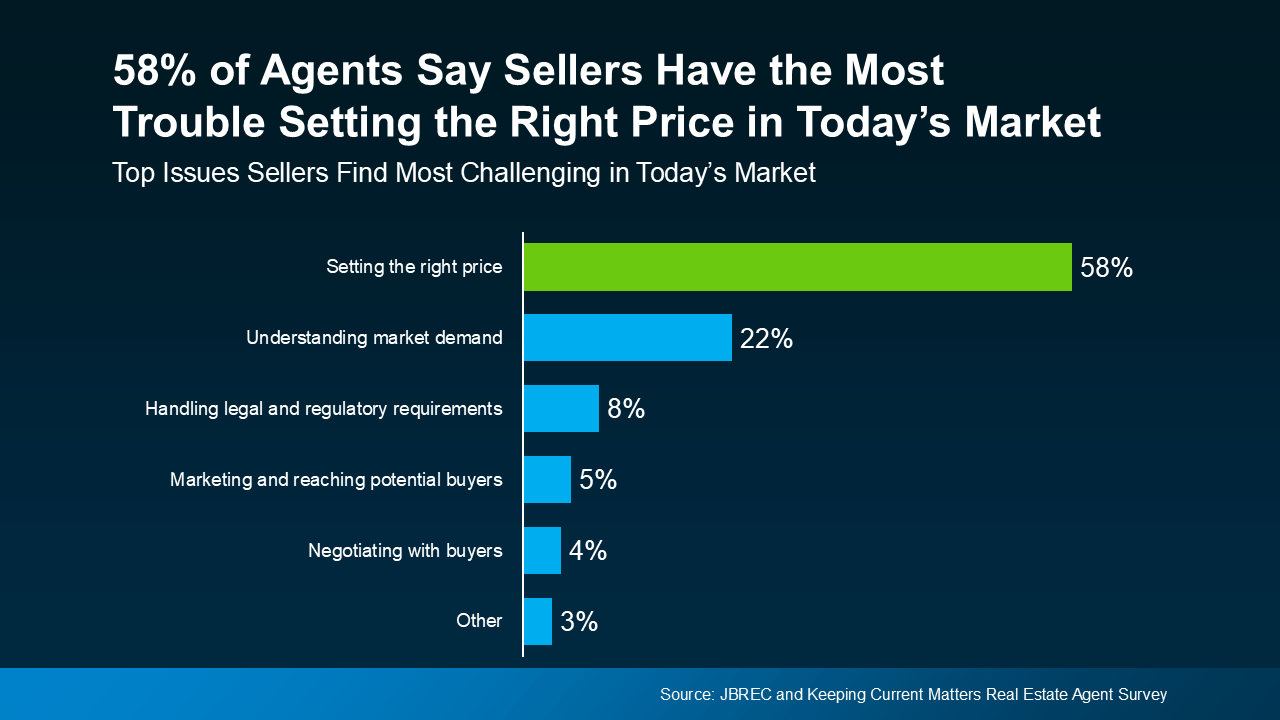

According to a survey by John Burns Real Estate Consulting (JBREC) and Keeping Current Matters (KCM), real estate agents agree the #1 thing sellers struggle with right now is setting the right price for their house (see graph below):

And more often than not, homeowners tend to overprice their listings. If you aren’t up to speed on what’s happening in your local market, you may give in to the temptation to price high so you can have as much wiggle room as possible to negotiate. You don’t want to do this.

And more often than not, homeowners tend to overprice their listings. If you aren’t up to speed on what’s happening in your local market, you may give in to the temptation to price high so you can have as much wiggle room as possible to negotiate. You don’t want to do this.

Today’s buyers are more cautious due to higher rates and tight budgets, and a price that feels out of reach will scare them off. And if no one’s looking at your house, how’s it going to sell? This is exactly why more sellers are having to do price cuts.

To avoid this headache, trust your agent’s expertise from day 1. A great agent will be able to tell you what your neighbor’s house just sold for and how that impacts the value of your home.

Another common mistake is trying to avoid doing work on your house. That leaky faucet or squeaky door might not bother you, but to buyers, small maintenance issues can be red flags. They may assume those little flaws are signs of bigger problems — and it could cost you when offers come in lower or buyers ask for concessions. As Investopedia says:

“Sellers who do not clean and stage their homes throw money down the drain. . . Failing to do these things can reduce your sales price and may also prevent you from getting a sale at all. If you haven’t attended to minor issues, such as a broken doorknob or dripping faucet, a potential buyer may wonder whether the house has larger, costlier issues that haven’t been addressed either.”

The solution? Work with your agent to prioritize anything you’ll need to tackle before the photographer comes in. These minor upgrades can pay off big when it’s time to sell.

Buyers today are feeling the pinch of high home prices and mortgage rates. With affordability that tight, they may come in with an offer that’s lower than you want to see. Don’t take it personally. Instead, focus on the end goal: selling your house. Your agent can help you negotiate confidently without letting emotions cloud your judgment.

At the same time, with more homes on the market, buyers have options — and with that comes more negotiating power. They may ask for repairs, closing cost assistance, or other concessions. Be prepared to have these conversations. Again, lean on your agent to guide you. Sometimes a small compromise can seal the deal without derailing your bottom line. As U.S. News Real Estate explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

Notice anything? For each of these mistakes, partnering with an agent helps prevent them from happening in the first place. That makes trying to sell your house without an agent’s help the biggest mistake of all.

Avoid these common mistakes by starting with the right plan — and the right agent. Let’s connect so you don’t fall into any of these traps.

The past few years have been challenging for homebuyers, especially with higher home prices and mortgage rates. And if you’re trying to buy a home, it’s easy to worry you won’t be able to find something in your budget.

But here’s what you need to know. The number of homes for sale has grown a whole lot lately and that’s true for both existing (previously lived-in) and newly built homes. Here’s a look at those two bright spots for buyers right now and why they may make it a bit easier to find the home you’re been looking for.

Data from Realtor.com says the number of existing homes for sale improved by an impressive 22% in 2024. And experts say your pool of options is expected to get even better this year. Forecasts show inventory is projected to grow another 11-15% by the end of this year (see graph below):

Here’s why this is so good for your search. If you haven’t seen a house with all the features you need, just know that, as the number of homes for sale grows, you’ll have more options to choose from. That means a better chance of finding a home that checks all your boxes. As Ralph McLaughlin, Senior Economist at Realtor.com, says:

Here’s why this is so good for your search. If you haven’t seen a house with all the features you need, just know that, as the number of homes for sale grows, you’ll have more options to choose from. That means a better chance of finding a home that checks all your boxes. As Ralph McLaughlin, Senior Economist at Realtor.com, says:

“It could be a particularly good time to get out into the market . . . you're going to have more choice. And that's not something that buyers have really had much over the past several years.”

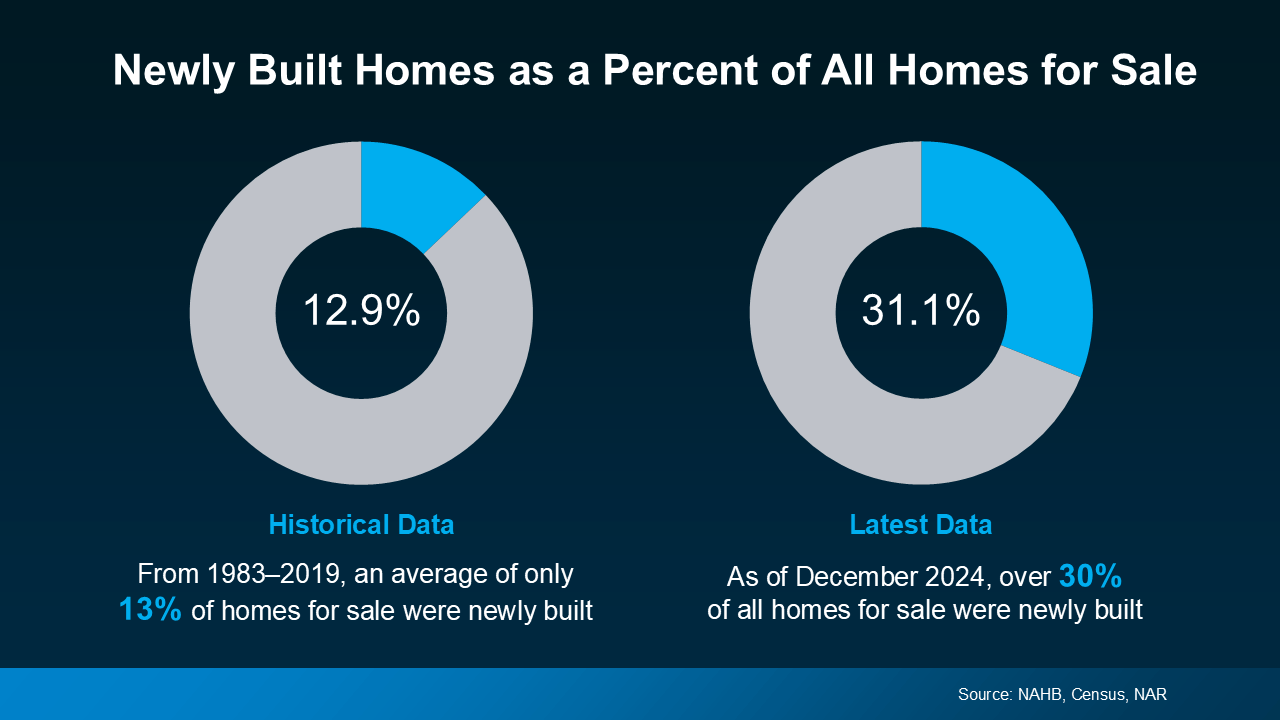

According to data from the Census and the National Association of Realtors (NAR), 31.1%, or roughly 1 in 3, homes on the market right now are newly built homes. That’s more than the norm (see charts below). But don't worry, that's not because builders are overdoing it – it’s just that they’re trying to catch up after years of underbuilding.

And the best part is, since builders have been focusing on smaller homes with lower price points, you may actually find out new builds are less expensive than you’d expect. So, while a lot of people write off new construction because it’s easy to assume the costs are way higher, lately, that price gap isn’t as big as you’d think. As CNET says:

And the best part is, since builders have been focusing on smaller homes with lower price points, you may actually find out new builds are less expensive than you’d expect. So, while a lot of people write off new construction because it’s easy to assume the costs are way higher, lately, that price gap isn’t as big as you’d think. As CNET says:

“If you live in an area where there's a lot of new construction happening . . . you might be able to purchase a new house for a price similar to or even less than a pre-owned one.”

If you haven’t been able to find a home that’s in your budget, it’s time to ask your agent about new builds. If you don’t, you may have been cutting your pool of options by about a third.

More choices could be the key to unlocking your homebuying goals in 2025. Reach out if you want to see what’s available in and around our area.

What features are you looking for in your next home? Let me know and I’ll put together a list of homes you’d love.

Displaying blog entries 1-8 of 8