Mt. Hood Real Estate Sales

Monday, October 19, 2009

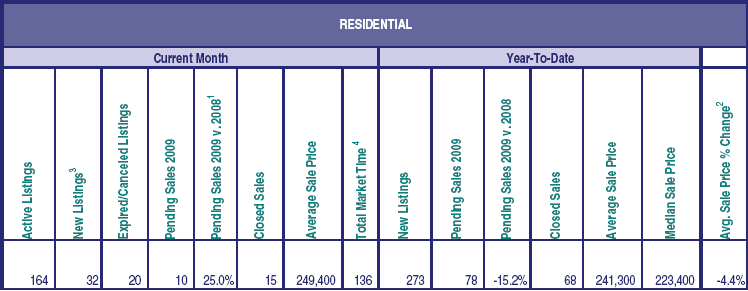

July and August pending sales proved to be substantial for the year with the biggest number of closings to date in September. It's been over a year since we have seen a monthly total of fifteen sales! Although there were none in the over $400.000 range, there were a few in the $300,000 area. Only one forest service cabin closed after the August flurry of sales. On a very positive note, only two of the fifteen sales were bank foreclosures.

Media reports indicate the third quarter of 2009 saw the greatest number of foreclousre filings yet. We are fortunate that the numbers of foreclosures have not hit levels in other states from 50 to 80% of their entire sales numbers.

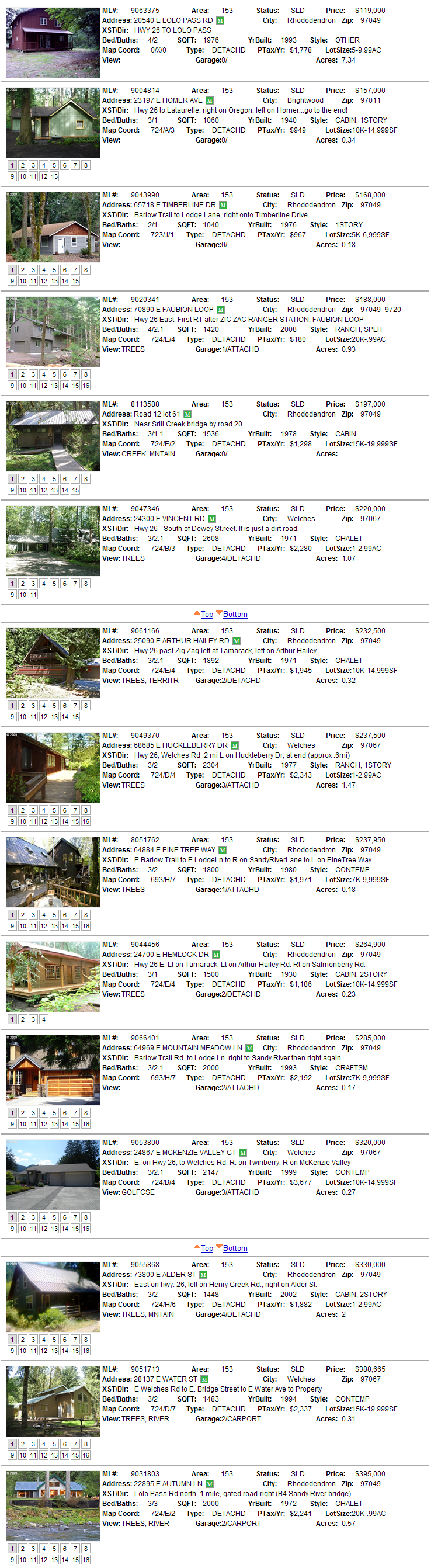

Here are September's sales:

Add Comment